Close Look: Why did AI tech pull markets higher?

What is the situation?

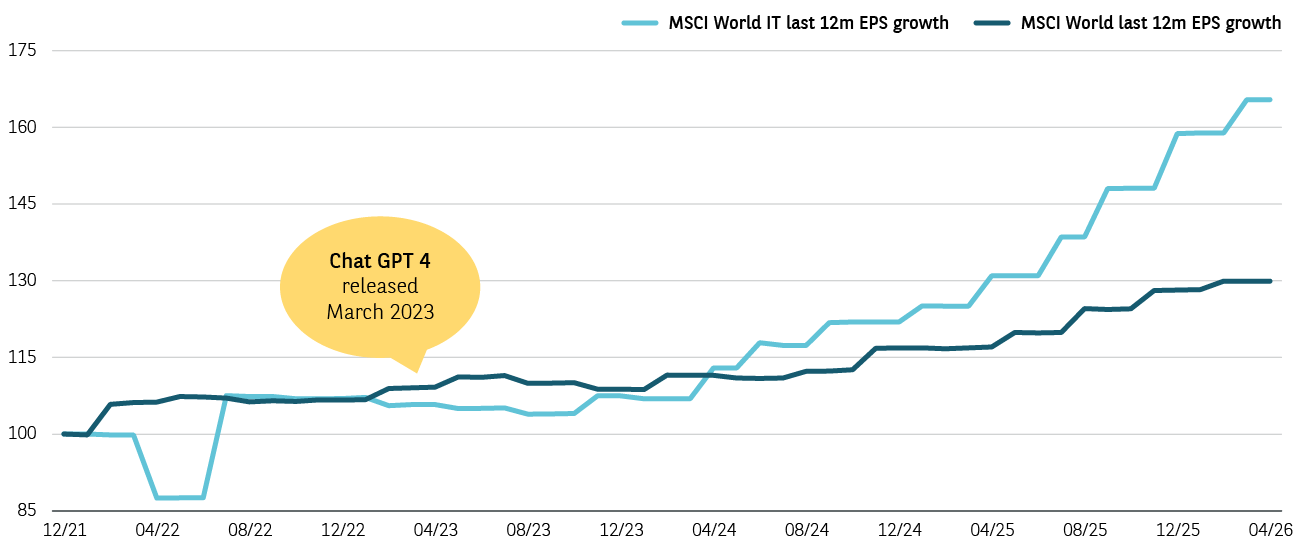

Since late March there has been a surge in equity markets which have a high exposure to tech hardware. In the US, the S&P 500 and the Nasdaq indices have touched new highs, while in Japan, the tech heavy Nikkei 225 has outperformed them both1. The new phenomenon driving markets has been hailed as ‘tech exceptionalism’ by some. This momentum trade buys into a surge in earnings growth within the sector, fired by the rollout of AI (artificial intelligence).

Cumulative 12 month earnings (US$) for MSCI World IT and MSCI World

Rebased 100 as of 31/12/2021

Source: Bloomberg, BNP Paribas Asset Management, 30 April 2026. Past performance is not a guide to future performance.

What is the background?

The so-called AI hyperscalers, that is Amazon, Meta, Microsoft and Google's parent Alphabet, have consistently upgraded AI capex spending plans over recent months. The collective total of planned spending for this year has jumped above US$700 billion2.

Anecdotally, the main beneficiaries of the California Gold Rush are said to have been the makers of picks and shovels. In much the same way, stocks that make tech hardware and semiconductors, are in hot demand. Indeed, the gains in the Philadelphia Semiconductor Index recently topped 70% year to date1.

The ‘AI everywhere’ investment theme is driving advances, including for old economy names, as the wave of investor enthusiasm gathers. Even the share price of US heavy truck manufacturer Caterpillar recently jumped, as its gas and diesel generators can be used as backup and primary power sources for AI data centres3.

Can AI tech sustain the rally?

The US enjoyed a strong Q1 earnings season, with average profits growth of 20% versus expectations of only 13%4. This significant ‘earnings beat’ was driven by the tech capex cycle, which so far appears to be resilient.

Newsflow from within the AI sector remains positive. As an example, AI giant Anthropic has successfully completed a fundraising round valuing the company at $900 billion5. Three months ago, the company was valued at $350bn5.

Add in expectations for major IPOs this year for SpaceX and OpenAI, and the tech sector might continue to power robust equity market performance.

What are the broader implications?

With an estimated 40% of US personal wealth in equities, recent market strength has boosted the ‘wealth effect’, with a knock on seen in better than expected US retail spending6. This in turn drives GDP growth forecasts, such as the Atlanta Fed's GDPNow, which was upgraded to 4% annualised growth for Q2 20267.

Within the context of stronger US growth, combined with a sharp jump in inflation due to energy price spikes, our economists believe that the chances of an increase in US interest rates have risen. The markets are expecting 30 basis points of rate hikes from the US Federal Reserve (Fed) by June 20278.

Expectations of higher interest rates have driven government bond yields higher. The yield on government bonds is used as a benchmark for the valuation of future earnings within equity markets. This could risk pushing valuation in the tech heavy sectors of the equity markets lower, if enthusiasm for the AI boom fades.

Our view

The rally in US equities has been particularly sharp. Nonetheless, we maintain a preference for US over European equities. We have also upgraded emerging market equities, seeking enhanced exposure to the global tech sector. Currently, the sources of growth are coming mainly from the technology sector, a trend which looks set to remain in place for the coming year. Europe seems unlikely to benefit from AI investments as much as the US or the emerging markets.

Elsewhere, the outcome of the current geopolitical situation remains uncertain, meaning that volatility of both economic and earnings growth forecasts is to be expected.

Sources: BNP Paribas Asset Management, as at 20 May 2026

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone. The company information mentioned (if any) is for informational purposes only and should not be construed as investment advice, a recommendation or solicitation.

- Source: Bloomberg, as at 18.05.2026

- Source: Bloomberg, as at 18.05.2026

- Source: Reuters, as at 30.04.2026

- Source: Financial Times, as at 04.05.2026

- Source: FactSet, as at 30.04.2026

- Source: Financial Times, as at 15.05.2026

- Source: Financial Times, as at 15.05.2026

- Source: BNP Paribas Asset Management, as at 18.05.2026

- Source: Atlanta Fed, as at 14.05.2026

- Source: CME, as at 20.05.2026